At first glance, the Strait of Hormuz looks like little more than a narrow strip of water between Iran and Oman. Yet over the past decade, markets have begun reacting to this corridor with increasing sensitivity — almost as if it were a financial indicator itself.

Oil jumps overnight. Bond yields swing violently. Gold rallies. Shipping insurers raise premiums. Equity markets rotate into defensive sectors. Traders suddenly begin discussing inflation persistence, central bank constraints, and reserve currency credibility.

Nothing may have happened in New York, London, Frankfurt, or Shanghai. Yet the entire financial system starts repricing risk because of tensions near Hormuz.

This is the deeper transformation markets are slowly recognizing:

The Strait of Hormuz is no longer merely an energy chokepoint. It has become a market regime indicator — a signal that reveals the underlying condition of globalization, monetary stability, geopolitical order, and systemic liquidity.

What markets are pricing is not simply the possibility of higher oil prices.

They are pricing the fragility of the global system itself.

The Artery of the Global Energy System

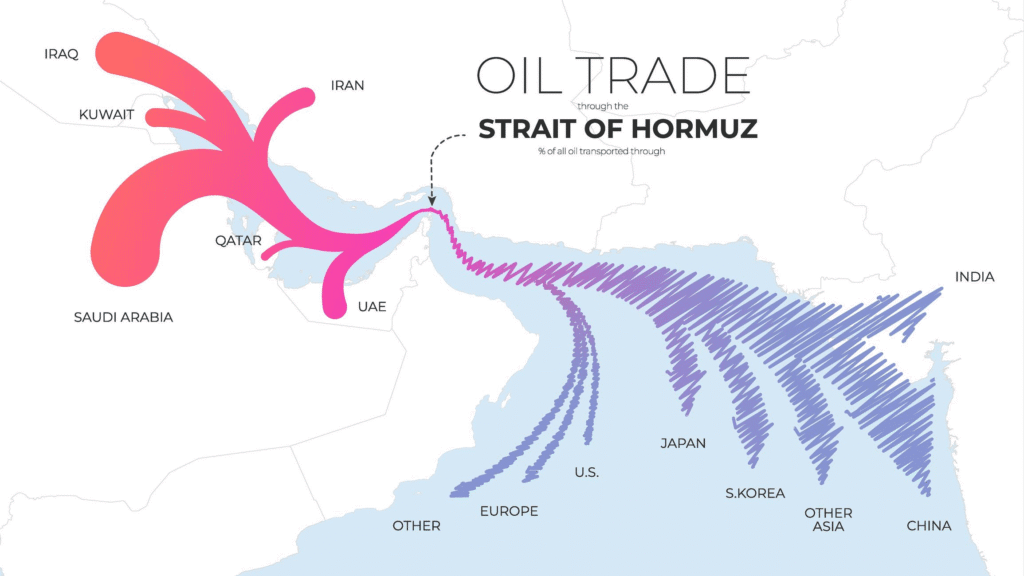

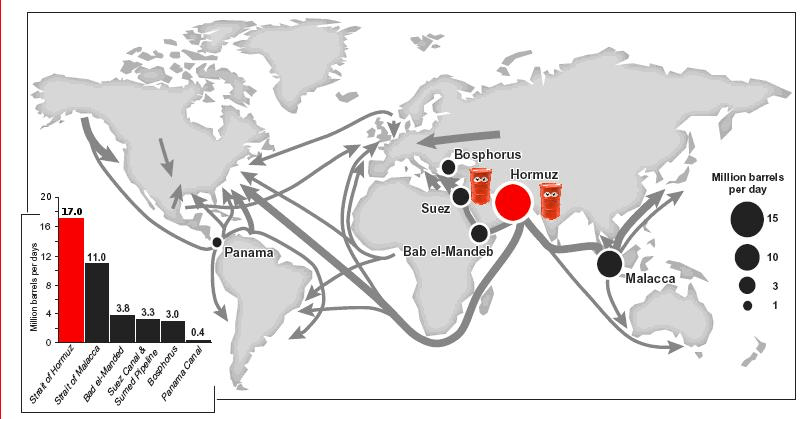

The Strait of Hormuz connects the Persian Gulf to the Gulf of Oman and the Arabian Sea. Through this narrow passage flows a massive portion of the world’s energy supply.

Major exporters including:

- Saudi Arabia

- Iraq

- United Arab Emirates

- Kuwait

- Qatar

- and Iran

depend heavily on this route for oil and LNG exports.

Roughly one-fifth of global oil consumption passes through Hormuz. Few logistical corridors on Earth carry such concentrated strategic importance. A disruption there does not merely affect one region — it transmits pressure directly into the foundation of the industrial economy.

Yet geography alone does not explain why markets now treat Hormuz as a macroeconomic signal rather than a regional risk.

The real change occurred inside the structure of the global economy itself.

The Old Market Regime: Temporary Oil Shock Thinking

For decades, geopolitical tensions in the Middle East were interpreted through a relatively simple framework.

Conflict near Hormuz meant:

- oil might spike temporarily,

- inflation could rise briefly,

- central banks might tighten slightly,

- and markets would eventually normalize.

The assumption underneath this framework was confidence.

Markets trusted:

- globalization,

- central bank credibility,

- stable supply chains,

- dollar dominance,

- and industrial resilience.

The world economy between the 1990s and late 2010s operated under a disinflationary regime. Cheap manufacturing, efficient logistics, expanding trade, and abundant liquidity absorbed geopolitical shocks with remarkable speed.

Even when oil surged, investors largely assumed the system itself remained intact.

Geopolitical instability was viewed as episodic noise rather than structural fragility.

Hormuz mattered, but it did not define the regime.

That changed after 2020.

The Collapse of the “Stable System” Assumption

The post-2020 world introduced a different reality entirely.

COVID exposed the brittleness of supply chains. Sanctions regimes became financial weapons. The war in Eastern Europe fragmented energy flows. Shipping routes became politicized. Inflation returned globally after decades of suppression. Sovereign debt burdens exploded while central banks struggled to maintain credibility.

Suddenly markets were no longer operating inside a stable globalization framework.

They were operating inside a fragmentation regime.

This distinction is critical.

In a stable globalization regime, a Hormuz disruption is a temporary oil problem.

In a fragmented regime, Hormuz becomes a signal that:

- supply chains are vulnerable,

- energy security is uncertain,

- inflation may become persistent,

- monetary policy may lose effectiveness,

- and geopolitical order itself may be deteriorating.

Markets now interpret Hormuz through the lens of systemic risk rather than commodity volatility.

That is why reactions have become larger, faster, and more cross-asset in nature.

Energy Is Not a Sector — It Is the Foundation

One of the biggest misconceptions in financial markets is the idea that energy belongs to a single economic sector.

Energy is not merely another industry.

It is embedded inside:

- transportation,

- food production,

- industrial manufacturing,

- military logistics,

- cloud infrastructure,

- shipping,

- mining,

- and global trade itself.

Every major inflationary episode in modern history has involved energy repricing.

When oil becomes unstable, the consequences spread far beyond gasoline prices. Freight costs rise. Production costs rise. Insurance costs rise. Food prices rise. Monetary expectations shift. Bond markets reprice future inflation risk.

This is why Hormuz matters far beyond oil traders.

The Strait functions as a pressure valve for the global industrial system.

When markets detect instability there, they begin questioning:

- future growth,

- future inflation,

- and the ability of policymakers to stabilize both simultaneously.

That combination is dangerous because it introduces stagflationary dynamics — the exact environment central banks are least equipped to manage.

Hormuz Exposes the Fragility of Globalization

Globalization optimized the world economy for efficiency.

Not resilience.

For decades, corporations pursued:

- lean inventories,

- just-in-time logistics,

- geographically concentrated manufacturing,

- and highly optimized trade routes.

These systems worked exceptionally well during periods of geopolitical stability.

But optimized systems often become fragile systems.

A single chokepoint disruption can suddenly affect:

- refinery flows,

- shipping insurance,

- manufacturing timelines,

- energy inventories,

- and national strategic reserves.

Markets increasingly understand that the global economy contains hidden structural vulnerabilities.

Most of the time those vulnerabilities remain invisible because liquidity masks them.

But during periods of stress, fragility emerges rapidly.

This resembles the logic behind Wyckoff Method.

In Wyckoff terms, stability often hides distribution underneath the surface. Markets appear calm until pressure accumulates enough to trigger a violent markdown phase.

Hormuz has become one of the catalysts capable of revealing that hidden instability.

The Limits of Central Banking

Modern markets spent decades believing central banks could manage nearly any crisis.

Financial crises?

Inject liquidity.

Recessions?

Cut rates.

Credit stress?

Expand balance sheets.

But geopolitical supply shocks expose the limitations of monetary policy.

Central banks can create money.

They cannot create:

- oil,

- shipping lanes,

- geopolitical trust,

- or physical security.

This distinction matters enormously.

Demand shocks can often be stabilized monetarily.

Supply shocks cannot.

If Hormuz tensions significantly restrict energy flows, policymakers face a brutal dilemma:

- tighten policy to control inflation and risk recession,

- or ease policy to protect growth and risk currency instability.

Either path damages confidence.

This is why modern Hormuz tensions increasingly trigger simultaneous moves across:

- bonds,

- commodities,

- currencies,

- gold,

- and equities.

Markets are no longer pricing an isolated commodity issue.

They are pricing policy paralysis.

The Dollar System Beneath Hormuz

The importance of Hormuz also extends into the structure of the international monetary system.

For decades, global oil trade reinforced dollar dominance through the petrodollar framework. Energy exports were largely denominated in USD, which created persistent global demand for dollar reserves and U.S. financial assets.

Military protection and monetary dominance became intertwined.

The United States effectively guaranteed maritime order while the dollar remained central to global trade settlement.

But fragmentation pressures are beginning to challenge that arrangement.

As geopolitical tensions rise, nations increasingly explore:

- bilateral trade agreements,

- non-dollar settlement systems,

- gold accumulation,

- and regional energy partnerships.

Markets now interpret instability near Hormuz as more than an energy threat.

It becomes a test of:

- American military credibility,

- dollar-centered financial architecture,

- and the durability of the post-Cold War order itself.

This is why every escalation around Hormuz increasingly intersects with discussions about:

- reserve currency transitions,

- sovereign debt credibility,

- and de-dollarization narratives.

The issue is no longer just oil supply.

It is confidence in the global system managing that supply.

Market Regimes Triggered by Hormuz

Modern markets increasingly rotate between distinct macro regimes depending on how geopolitical stress evolves.

Hormuz has become one of the triggers capable of accelerating those transitions.

1. Risk-Off Regime

In the early stages of escalation:

- oil rises,

- equities weaken,

- volatility expands,

- gold rallies,

- and capital rotates defensively.

Liquidity contracts as portfolio managers reduce leverage and hedge uncertainty.

This phase resembles a classic fear regime.

2. Inflationary Commodity Regime

If tensions persist, markets begin pricing structural scarcity.

Narratives shift toward:

- energy shortages,

- supply fragmentation,

- persistent inflation,

- and commodity supercycles.

Capital starts rotating toward:

- energy producers,

- commodities,

- shipping,

- defense,

- and hard assets.

The market transitions from panic to repricing.

3. Monetary Disorder Regime

The most dangerous phase emerges when energy instability combines with:

- excessive sovereign debt,

- monetary expansion,

- weakening reserve currency confidence,

- and geopolitical fragmentation.

At this stage, markets begin questioning the credibility of fiat systems themselves.

Gold strengthens not merely as a hedge against inflation, but against institutional uncertainty.

Even digital assets begin attracting narratives around monetary distrust and capital escape.

Hormuz tensions alone do not create this regime.

But they can accelerate recognition that the regime already exists.

The Wyckoff Interpretation of Geopolitical Stress

One of the most fascinating aspects of market behavior is that institutions often reposition long before mainstream narratives emerge.

This aligns closely with Wyckoff principles.

Markets rarely collapse because of a headline alone.

The headline usually acts as the catalyst that reveals positioning already taking place beneath the surface.

In many cases:

- energy sectors strengthen quietly,

- bond duration exposure declines,

- commodity positioning builds,

- and defensive rotation begins

before the public fully understands why.

By the time media attention centers on Hormuz, institutional campaigns may already be advanced.

The geopolitical event becomes the visible trigger for a structural process that started much earlier.

This is why understanding market regimes matters more than reacting emotionally to headlines.

The real signal often appears inside positioning and liquidity behavior before it appears in the news cycle.

Historical Moments That Changed Market Psychology

The transformation of Hormuz into a regime indicator did not happen overnight.

It emerged gradually through repeated systemic shocks.

The 1973 Oil Crisis

The 1973 oil shock introduced the modern world to stagflation:

- rising inflation,

- slowing growth,

- monetary instability,

- and energy vulnerability.

Markets learned that energy disruptions could reshape entire economic regimes.

The Tanker War of the 1980s

During the Iran-Iraq conflict, attacks on Gulf shipping highlighted the vulnerability of maritime energy flows.

Yet globalization was still expanding and markets largely retained faith in the broader system.

The psychological regime remained stable.

The 2019 Saudi Aramco Attack

The attack on facilities linked to Saudi Aramco became a critical turning point.

Markets suddenly recognized how vulnerable modern energy infrastructure had become to asymmetric disruption.

The realization was profound:

extremely sophisticated global systems could be destabilized by relatively localized events.

The Post-2022 Fragmentation Era

After 2022, markets entered a structurally different environment:

- sanctions intensified,

- trade routes shifted,

- energy blocs formed,

- reserve diversification accelerated,

- and geopolitical alignment increasingly shaped capital flows.

This was the environment in which Hormuz evolved from a regional concern into a systemic market signal.

The Psychological Dimension of Hormuz

Markets do not trade reality directly.

They trade expectations, probabilities, and fear.

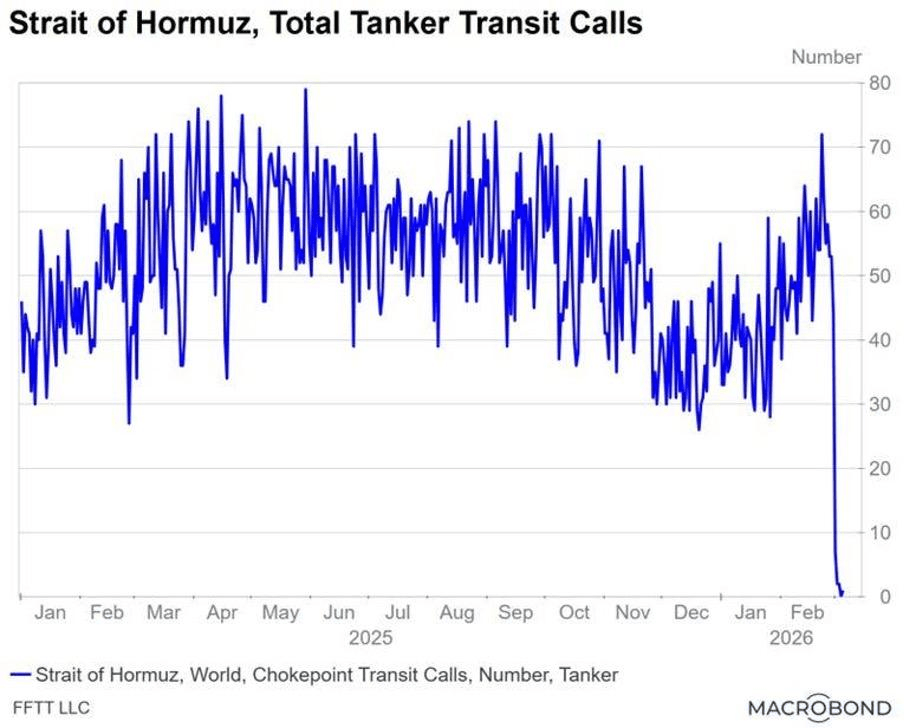

This means the actual closure of Hormuz may matter less than the perception that closure is possible.

Uncertainty itself becomes destabilizing.

When traders cannot confidently model:

- inflation trajectories,

- supply chain continuity,

- policy responses,

- or geopolitical escalation,

risk premiums expand rapidly.

This creates reflexive feedback loops similar to those described by George Soros.

Fear changes behavior:

- companies increase inventories,

- investors hedge aggressively,

- insurers raise premiums,

- governments intervene,

- and volatility begins feeding itself.

The expectation of disruption can partially create the disruption.

Why This Matters Going Forward

The significance of Hormuz today is not simply military or geopolitical.

It is civilizational.

The modern financial system depends on assumptions of continuity:

- stable trade,

- stable energy,

- stable currencies,

- and stable geopolitical order.

Hormuz sits at the intersection of all four.

That is why markets increasingly treat it as a regime indicator rather than an isolated risk event.

The Strait reveals how dependent globalization became on uninterrupted stability — and how fragile confidence becomes when that stability is questioned.

In the end, what flows through Hormuz is not just oil.

It is confidence in the architecture of the global order itself.